Author’s note: This is my own quantitative study of long-term investing in the S&P 500 index, comparing three approaches: regular dollar-cost averaging, “buying the dips” using pre-defined drop dates, and leaving money in a savings account.

Strategy Variants

In this study, I compared the following three strategies, each starting from the same monthly cash flow of $500:

- Strategy 1 – Regular Monthly Investing (DCA): Invest $500 every month into the S&P 500, regardless of market conditions (classic Dollar Cost Averaging).

- Strategy 2 – “Buy the Dip” + Interest: Save $500 every month into a 5% savings account, and invest the accumulated cash into the S&P 500 only on automatically detected market drop dates.

- Strategy 3 – Pure Savings: Save $500 every month in a savings account at 5% annual interest, without investing in the stock market.

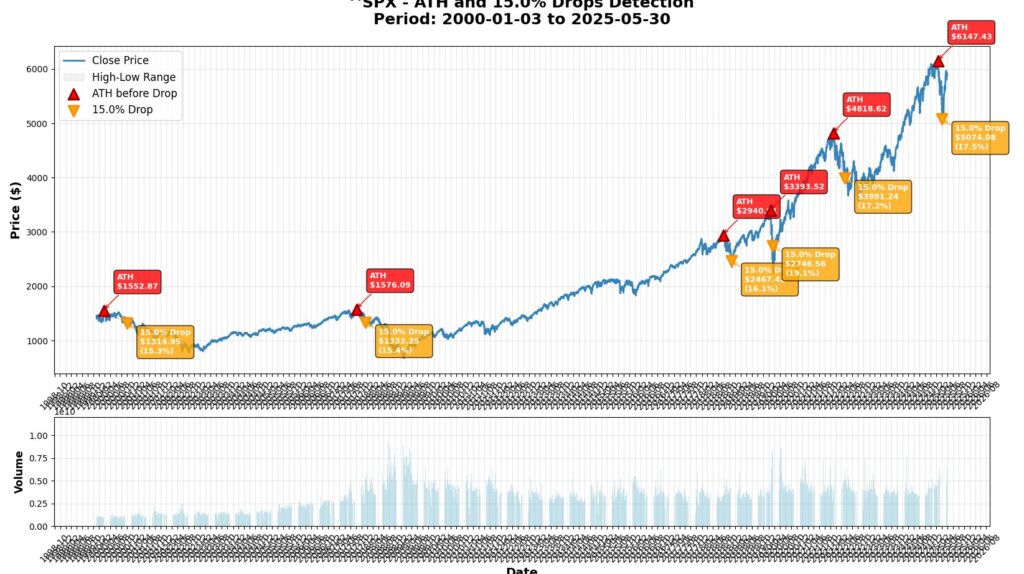

The market drop dates for Strategy 2 were detected automatically using my proprietary automation tool:

2000-11-30, 2008-01-17, 2018-12-20, 2020-03-09, 2022-05-09, 2025-04-04

Important note: This type of strategy is designed for broad stock indices, which historically tend to rise over the long term. For individual stocks, the risk of permanent loss is much higher because companies can be delisted or go bankrupt.

Numerical Results

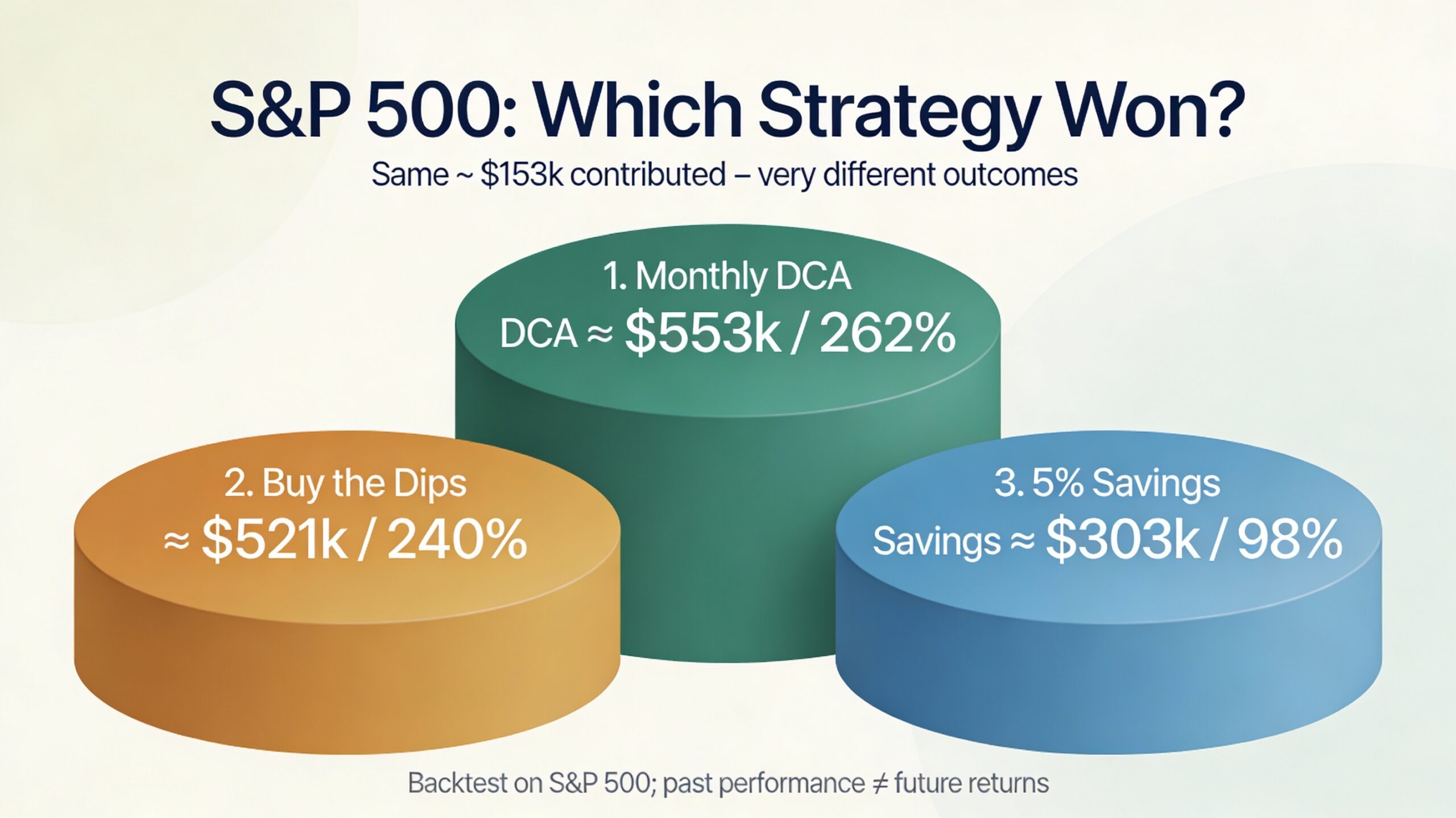

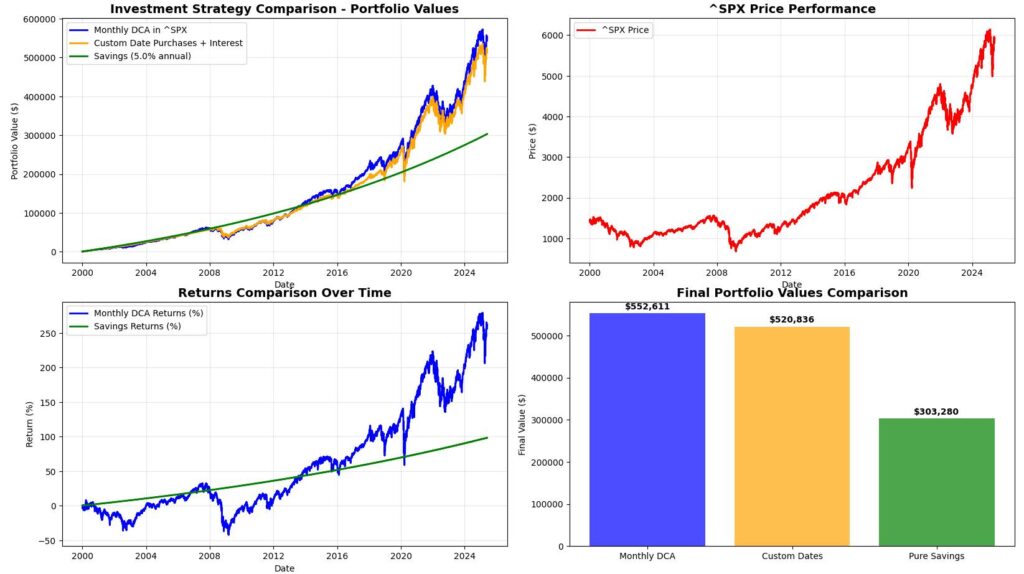

Strategy 1 – Regular Monthly DCA

- Total invested: $152,500.00

- Final portfolio value: $552,611.33

- Total return: 262.37%

- Profit: $400,111.33

Strategy 2 – Custom Date Purchases + Interest

- Total deposits: $153,000.00

- Final portfolio value: $520,835.75

- Total return: 240.42%

- Profit: $367,835.75

Strategy 3 – Pure 5% Savings Account

- Total deposits: $153,000.00

- Final account value: $303,279.87

- Total return: 98.22%

- Profit: $150,279.87

Key Takeaways

1. Stocks vs. Savings

- The regular DCA strategy achieved a 262.37% return versus 98.22% for the savings-only strategy.

- In absolute terms, stock investing generated $249,832 more profit than the savings account.

- Even with a relatively attractive 5% interest rate, long-term savings in cash lagged far behind the stock market.

2. DCA vs. “Buying the Dip”

- Regular monthly investing (DCA) produced the best result: 262.37% total return.

- The selective “buy the dip” strategy reached 240.42% – good, but still behind DCA.

- The difference in profit between the two stock strategies was $31,776 in favour of regular DCA.

3. Value of Discipline

- Automatic, rule-based investing removes emotions and the need to predict short-term market moves.

- Trying to pick “better moments” to invest (market timing) underperformed a simple, mechanical plan.

- DCA helps smooth out volatility and keeps the investor continuously in the market.

4. Power of the Long Term

- Both stock-based strategies significantly outperformed the pure savings approach over the tested period.

- The combination of compounding and long-term market growth was a major driver of results.

- Even the weaker stock strategy (240.42%) still beat savings by about 142 percentage points.

5. Practical Implications for Investors

- Simplicity wins: A regular monthly investment into a broad index fund was the top-performing strategy in this study.

- You do not need to be a market expert; consistent behaviour and discipline mattered more than timing.

- This kind of strategy is most suitable for long horizons, likely 10+ years.

Final Thoughts

For an average long-term investor, a simple DCA plan into a broad index such as the S&P 500 appears to be both easy to implement and highly effective in this historical test. It outperformed both trying to time the market and staying entirely in a savings account.

These results are based on a specific historical period and a particular rule set, so future outcomes may differ. However, the underlying principles of diversification, discipline, and long-term investing remain highly relevant.