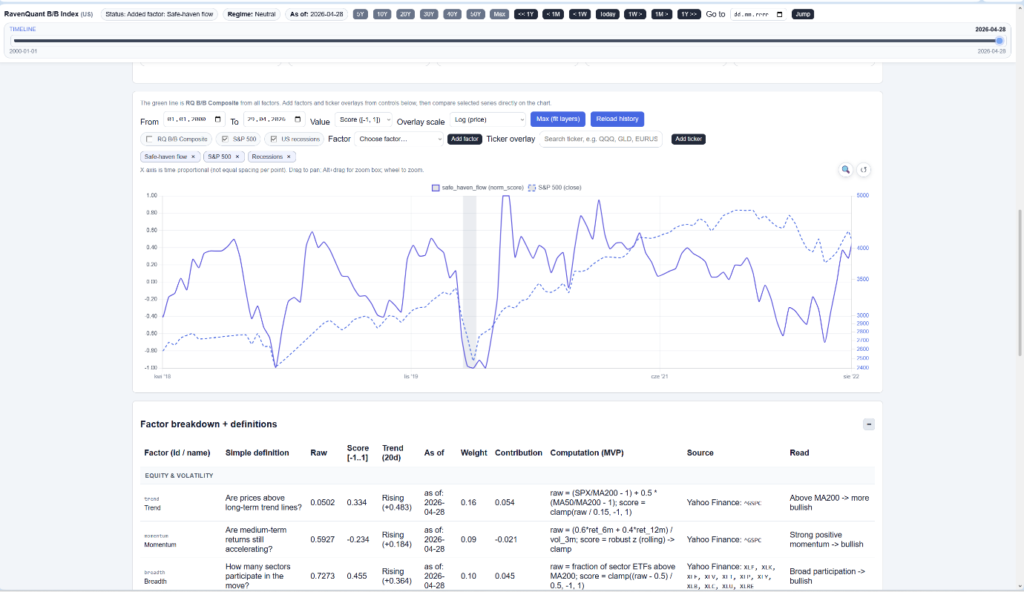

Live dashboard: RavenQuant B/B Index

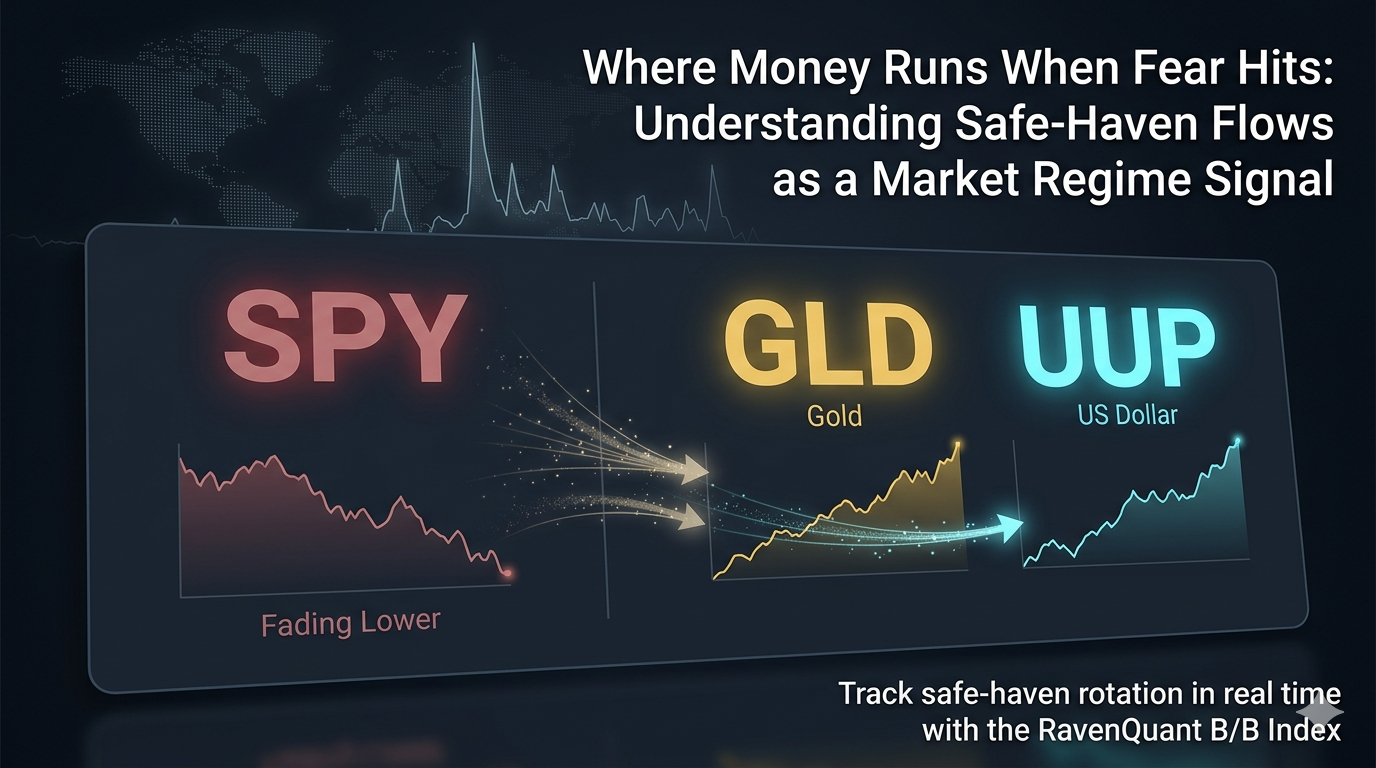

Safe-Haven Flows is a key market regime signal for investors. Ask anyone who has traded through a genuine risk-off event — not a routine 3% pullback, but the kind of episode where screens go red for days and nobody seems to know where the floor is — and they’ll tell you the same thing: you can feel the rotation happening in real time. Capital leaves the risky stuff and moves toward the perceived safe stuff, often with a speed and conviction that is itself telling. The question is how to measure that rotation systematically rather than trying to feel it qualitatively.

The answer lies in relative performance. By tracking how the S&P 500 (SPY) performs versus two canonical safe-haven assets — gold (GLD) and the US dollar (UUP) — you get a continuous, data-driven read on where capital is flowing. When equities are outperforming safe havens on a sustained basis, the regime is risk-on. When gold and the dollar are attracting money at equities’ expense, the regime is risk-off. The relative performance window filters day-to-day noise and focuses on the kind of sustained directional flows that mark actual regime shifts rather than one-day squalls.

What Safe-Haven Rotation Reveals About Market Stress

Gold’s role as a safe-haven asset is well-established over centuries, though the precise mechanism is sometimes misunderstood. Gold doesn’t have a yield, a cash flow, or a business behind it. What it has is a history of holding purchasing power when faith in fiat money or institutions is shaking. In genuine financial crises — when sovereign debt risks rise, when inflation runs hot, when geopolitical stress intensifies — investors reach for gold as a store of value outside the financial system.

But gold’s safe-haven behavior is not unconditional. The March 2020 episode is the most instructive recent case study. In the initial days of the COVID market crash — roughly March 12 through 16 — gold dropped alongside equities. This wasn’t irrational panic; it was a liquidity crisis. When margin calls hit and everyone simultaneously needed cash, investors sold whatever had liquidity and a bid, including gold ETFs. The safe-haven premium didn’t kick in until after the Federal Reserve announced emergency interventions and the acute liquidity crisis was addressed. Gold then surged while equities were still finding their footing.

This is exactly why a rolling relative performance window works better than a day-one reaction. You’re trying to capture sustained rotation into safe havens, not the chaotic first hours of a market panic.

Why the US Dollar Strengthens During Global Risk-Off

For investors outside the United States, the dollar’s safe-haven status can seem puzzling. The US runs persistent deficits, the national debt is enormous, and the dollar has long been expected by some observers to eventually lose its reserve currency status. Yet in virtually every major global risk-off episode of the past thirty years, the dollar strengthens. Why?

The answer lies in the structure of global dollar-denominated debt. A vast amount of lending globally — to emerging market governments, to corporations in developing countries, to financial institutions worldwide — is denominated in US dollars. The Bank for International Settlements has documented this extensively in its quarterly reviews at bis.org. When stress hits and institutions need to cover positions or repay dollar-denominated obligations, they must buy dollars in the foreign exchange market regardless of their view on US fundamentals. This creates a systematic, mechanical demand for the dollar precisely when conditions are worst.

UUP, the Invesco DB US Dollar Index Bullish Fund, provides a clean, liquid daily-priced proxy for dollar strength. It tracks a basket of dollar-versus-major-currencies positions and is available through Yahoo Finance without the complexity of running FX futures positions.

When Safe-Haven Correlations Break: Lessons From 2022

The conventional risk-off framework — equities fall, bonds rise, gold rises, dollar strengthens — broke down in 2022 in a way that was genuinely unusual. Stocks fell 20%+. Bonds fell too (10-year Treasury prices fell roughly 16% as yields rose sharply from 1.5% to over 4.5%). Gold was essentially flat for the year. But the dollar, as measured by UUP, surged dramatically — the DXY dollar index hit its highest level since the early 2000s.

It was a year of dollar safe-haven demand but almost nothing else behaving “normally.” The driver was the fastest Federal Reserve tightening cycle in modern history, combined with the US economy holding up better than Europe (facing an energy crisis from the Russia-Ukraine war) and Japan (maintaining yield curve control). The dollar was the only liquid global safe haven left standing. An approach that only watched gold would have badly misread the regime in 2022. Including the dollar alongside gold captured the genuine safe-haven dynamic even when gold failed to play its typical role.

Why Relative SPY-GLD-UUP Performance Filters Noise

The choice to measure relative performance of equities versus safe havens — rather than watching each in absolute terms — reflects a deliberate approach to filtering noise. Both gold and the dollar can move for reasons unrelated to equity market stress. Gold responds to inflation expectations, Chinese demand, mining supply dynamics. The dollar responds to relative interest rate differentials, trade flows, and capital account dynamics. By anchoring the reading in how these assets perform relative to equities specifically, you filter out much of that non-equity-related noise.

Using ETFs rather than futures or spot rates also matters for data cleanliness. SPY, GLD, and UUP are among the most liquid instruments in global markets, priced daily, with clean historical data accessible through sources like Yahoo Finance. No futures rolling adjustments, no overnight spot rate complications — just closing prices.

The limitation is real and worth acknowledging: gold and the dollar don’t always move independently of each other. Gold tends to move inversely to the dollar in non-stressed environments because of simple correlation dynamics — a stronger dollar makes dollar-denominated gold more expensive in other currencies, suppressing demand. A rolling relative-performance window is designed to distinguish between these normal correlation-driven moves and the synchronized rush to both assets that characterizes genuine global risk-off episodes.

Flows in RavenQuant in Real Time

If you want to track the current safe-haven flow reading — whether capital has been rotating toward or away from gold and the dollar relative to equities — it’s one of the factors in the RavenQuant B/B Index at ravenquant.com. It tends to move sharply during exactly the episodes that matter most, and watching its 20-day trend alongside credit spread and volatility readings is one of the cleaner ways to gauge whether a pullback is a routine drawdown or the beginning of something more structural.

Explore the live index here: https://bull-bear-analyzer-production.up.railway.app